Appraisal Insights

-

February 11, 2024

Conventional Loan Interest Rates

Demystifying conventional loan interest rates! Discover how credit score, market conditions, and more impact your rates.

Demystifying conventional loan interest rates! Discover how credit score, market conditions, and more impact your rates.

When considering a conventional loan, it's important to understand how interest rates play a significant role in the overall cost of borrowing. This section provides an overview of conventional loans and the role that interest rates play in this type of financing.

Conventional loans are mortgage loans that are not insured or guaranteed by a government agency such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). These loans are typically offered by private lenders, such as banks or credit unions, and are subject to the lender's guidelines and requirements.

Conventional loans offer various loan terms and down payment options, making them a popular choice for borrowers who meet the lender's eligibility criteria. The interest rates on conventional loans can vary depending on several factors, including the borrower's creditworthiness, loan-to-value ratio, and market conditions.

Interest rates are the cost of borrowing money and are expressed as a percentage of the loan amount. In the case of conventional loans, interest rates can significantly impact the total amount paid over the life of the loan.

The interest rate on a conventional loan is determined by several factors, including market conditions, the borrower's creditworthiness, and the loan's specific terms. Lenders assess the borrower's financial profile, including credit score, income, and employment history, to determine the risk associated with lending to an individual.

Lenders offer different interest rates based on the level of risk they perceive. Borrowers with higher credit scores and lower risk profiles generally qualify for lower interest rates, while those with lower credit scores or higher risk profiles may be offered higher interest rates.

Understanding the factors that affect conventional loan interest rates is crucial for borrowers. By improving their credit score, maintaining a low loan-to-value ratio, and monitoring market conditions, borrowers can potentially secure more favorable interest rates. Additionally, shopping around for lenders and considering options such as paying points or locking in the rate at the right time can help borrowers secure the best possible interest rates on their conventional loans.

By comprehending the fundamentals of conventional loans and the impact of interest rates, borrowers can make informed decisions when it comes to financing their home purchases or refinancing their existing mortgages.

When it comes to conventional loans, interest rates play a significant role in determining the cost of borrowing. Several factors influence these interest rates, and understanding them is crucial for borrowers. Let's explore the key factors that affect conventional loan interest rates: credit score, loan-to-value ratio, loan term, and market conditions.

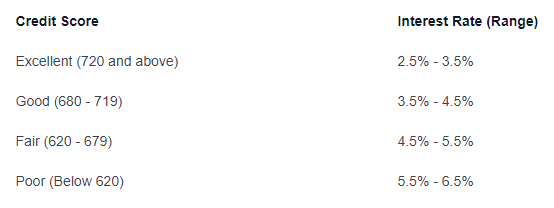

One of the most influential factors in determining the interest rate for a conventional loan is the borrower's credit score. Lenders assess the creditworthiness of borrowers based on their credit scores, which reflect their past credit history and repayment behavior. A higher credit score indicates a lower risk for the lender, which often results in a more favorable interest rate for the borrower.

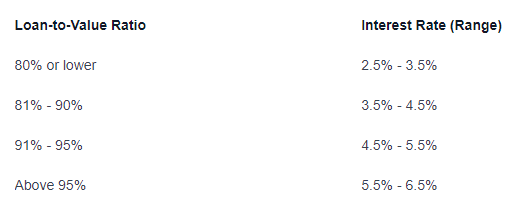

The loan-to-value (LTV) ratio is another factor that impacts conventional loan interest rates. The LTV ratio represents the loan amount compared to the appraised value or purchase price of the property, whichever is lower. A lower LTV ratio indicates a lower risk for the lender, as there is more equity in the property. This typically results in more favorable interest rates for borrowers with a lower LTV ratio.

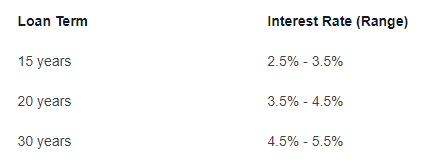

The loan term, or the length of time borrowers have to repay their conventional loans, also influences interest rates. Typically, shorter loan terms come with lower interest rates compared to longer terms. This is because lenders are taking on less risk over a shorter period. However, it's important to note that shorter loan terms may result in higher monthly payments.

Interest rates for conventional loans are also influenced by market conditions, including factors such as inflation, economic indicators, and the overall demand for loans. These factors can cause interest rates to fluctuate over time. Borrowers should stay informed about current market conditions and consult with mortgage professionals to understand how market trends may impact their interest rates.

Understanding the factors that affect conventional loan interest rates empowers borrowers to make informed decisions. By improving their credit scores, maintaining a lower loan-to-value ratio, selecting an appropriate loan term, and staying informed about market conditions, borrowers can increase their chances of securing the most favorable interest rates available to them.

When it comes to conventional loans, borrowers have the option to choose between two types of interest rates: fixed interest rates and adjustable interest rates. Understanding the differences between these two options is crucial in making an informed decision about your loan.

Fixed interest rates are the most common type of interest rates for conventional loans. As the name suggests, these rates remain fixed or constant throughout the entire loan term. This means that your monthly mortgage payment will remain the same over the life of the loan.

One of the advantages of fixed interest rates is the predictability they offer. With a fixed rate, you can budget your finances with confidence, as your mortgage payment will not fluctuate due to changes in interest rates. This stability can provide peace of mind, especially in times when interest rates are expected to rise.

Here's a comparison of fixed interest rates for different loan terms:

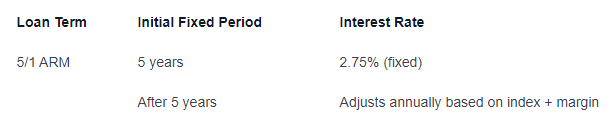

Unlike fixed interest rates, adjustable interest rates, also known as adjustable-rate mortgages (ARMs), can change over time. These rates are typically fixed for an initial period, often 3, 5, 7, or 10 years, and then adjust periodically based on market conditions.

The initial fixed period of an adjustable interest rate provides borrowers with a lower rate compared to fixed interest rates. However, once the initial period ends, the interest rate can adjust annually or semi-annually. The adjustment is usually based on a specific index, such as the U.S. Treasury Bill rate or the London Interbank Offered Rate (LIBOR), plus a margin determined by the lender.

Adjustable interest rates are suitable for borrowers who plan to stay in their home for a shorter period or anticipate changes in their financial situation. However, it's important to carefully consider the potential risks associated with adjustable rates, as they can result in higher mortgage payments if interest rates rise significantly.

Here's an example of an adjustable interest rate structure:

Understanding the pros and cons of fixed and adjustable interest rates is crucial when choosing a conventional loan. It's essential to evaluate your financial goals, risk tolerance, and future plans to determine which option aligns best with your needs. Consulting with a mortgage professional can provide further guidance and help you make an informed decision.

When it comes to securing a conventional loan, getting the best interest rates is a top priority for borrowers. Here are some strategies to help you obtain favorable interest rates on your conventional loan.

One of the most influential factors in determining your interest rate is your credit score. Lenders consider borrowers with higher credit scores to be less risky, resulting in lower interest rates. To improve your credit score:

By consistently practicing good credit habits, you can boost your credit score and increase your chances of qualifying for lower interest rates.

Not all lenders offer the same interest rates on conventional loans. It's essential to shop around and compare offers from different lenders to find the most competitive rates. Obtain quotes from multiple lenders, including banks, credit unions, and online lenders. Carefully review the loan terms, including interest rates, fees, and closing costs, to make an informed decision.

Paying points, also known as discount points, can be an effective strategy to lower your interest rate. Points are prepaid interest that you pay upfront to reduce the interest rate over the life of the loan. Each point typically costs 1% of the loan amount and can lower the interest rate by a certain percentage.

Consider your financial situation and how long you plan to stay in the home. If you anticipate being in the property for an extended period, paying points upfront could result in significant savings over time. However, it's important to calculate whether the upfront cost of points aligns with your long-term financial goals.

Interest rates can fluctuate, so it's crucial to lock in your rate once you've found a favorable one. Interest rate locks are agreements between the borrower and the lender that guarantee a specific interest rate for a certain period, typically 30 to 60 days. This protects you from potential rate increases during the loan processing period.

Ensure that you have all the necessary documentation and information ready to expedite the loan process. Discuss the rate lock period with your lender to ensure it aligns with your closing timeline. Keep in mind that some lenders may charge a fee for rate locks, so be sure to inquire about any associated costs.

By following these strategies, you can increase your chances of securing the best interest rates on your conventional loan. Remember to be proactive in improving your credit score, compare offers from multiple lenders, consider paying points, and lock in your rate to maximize your savings over the life of the loan.

To make informed decisions about conventional loans, it's essential to stay up-to-date with the latest information regarding interest rates. By monitoring market trends, consulting with mortgage professionals, and exploring refinancing options, borrowers can navigate the landscape of conventional loan interest rates more effectively.

Keeping an eye on market trends is crucial when it comes to understanding conventional loan interest rates. These rates can fluctuate based on various factors, including economic conditions, inflation rates, and the overall state of the housing market. By staying informed about market trends, borrowers can gauge whether interest rates are rising, falling, or remaining stable.

Monitoring market trends can be done through financial news sources, online resources, and professional insights. Being aware of shifts in interest rates allows borrowers to time their loan applications more strategically and potentially secure a more favorable rate.

When it comes to conventional loan interest rates, consulting with mortgage professionals can provide valuable expertise and guidance. Mortgage brokers, loan officers, and financial advisors have in-depth knowledge of the lending industry and can offer personalized insights based on the borrower's financial situation.

Mortgage professionals can help borrowers understand the current interest rate landscape, provide information on lender-specific rates, and guide them through the loan application process. They can also assist in analyzing the borrower's financial profile and identifying opportunities for securing more favorable interest rates.

For borrowers who already have a conventional loan, refinancing can be an option to take advantage of lower interest rates. Refinancing involves replacing an existing loan with a new loan, usually to obtain better terms, such as a lower interest rate.

Refinancing allows borrowers to adjust their loan's interest rate and potentially reduce their monthly mortgage payments. However, it's important to consider factors such as closing costs, loan terms, and the length of time the borrower plans to stay in the property before deciding to refinance.

Borrowers should evaluate their financial goals, compare current interest rates with their existing loan terms, and assess the potential benefits and costs of refinancing. Consulting with mortgage professionals can provide valuable insights and help borrowers determine if refinancing is the right choice for their specific circumstances.

By staying informed about market trends, seeking professional advice, and considering refinancing options, borrowers can stay ahead of changes in conventional loan interest rates. This knowledge empowers borrowers to make well-informed decisions, potentially saving them money over the life of their loan.

When it comes to securing a conventional loan, understanding the factors that influence interest rates is crucial. By improving credit scores, maintaining a lower loan-to-value ratio, selecting an appropriate loan term, and staying informed about market conditions, borrowers can increase their chances of securing the most favorable interest rates available to them.

Choosing between fixed and adjustable interest rates requires careful consideration of personal financial goals and risk tolerance. Fixed interest rates offer predictability and stability, while adjustable interest rates may provide lower initial rates for shorter-term homeowners.

To get the best interest rates on conventional loans, borrowers should improve their credit score, shop around for lenders, consider paying points upfront to reduce the rate over time and lock in the rate once they find a favorable one.

Staying informed about market trends and consulting with mortgage professionals can also provide valuable insights into navigating conventional loan interest rates. With these strategies in mind, borrowers can make well-informed decisions that align with their financial goals and potentially save them money over the life of their loan.